Adrian Buss, Associate Professor of Finance at INSEAD explains the impact of institutional investors on informational efficiency here, an aspect relevant to participants in today’s financial markets

The importance of institutional investors in financial markets has increased considerably over the last decades. For example, while financial institutions, such as mutual funds, pension funds, hedge funds, banks and insurance companies, owned only 7% of all U.S. equity in 1950, today they account for about 80% of equity ownership. Moreover, they are responsible for a majority of the transactions in today’s financial markets.

Notably, the objectives of these institutional investors differ from those of traditional households. While both try to manage their funds to maximise portfolio returns, institutional investors are usually also concerned about their performance relative to a benchmark (often a stock-market index). Such benchmarking concerns arise from the observation that financial institutions who beat their benchmark attract considerably more capital from clients in the future. This, in turn, increases future management fees and, hence, future profits. Benchmarking concerns also arise from explicit performance fees. Specifically, to align the incentives of fund managers and their clients, asset-management contracts often specify that managers get paid higher fees if they outperform their benchmark.

This practice of benchmarking can have a substantial impact on financial-market equilibrium because – due to their sheer size – institutional investors often act as the “marginal investor.” However, while the impact of benchmarking on asset prices has been studied before (see, e.g., Cuoco and Kaniel (2011) and Basak and Pavlova (2013)), benchmarking might also affect the informational role of financial markets, that is, their ability to aggregate and disseminate information. Intuitively, investors continuously try to obtain “private information” (i.e., information not available to others) by studying financial statements or uncovering information about consumers’ tastes or macro-economic trends; with the goal of generating trading profits and, hence, high portfolio returns.

Whenever an investor uses such private information in his or her trading, part of the information gets incorporated into stock prices. For example, if an investor – following positive (negative) firm-specific news – buys (sells) shares of a company, the firm’s stock price goes up (down) which, in turn, reveals part of the investor’s information to other investors. Thus, by tracking stock-price movements in financial markets, investors can infer private information that other investors possess. The degree to which prices incorporate and reveal information is called informational efficiency and is of foremost importance because it determines the efficient allocation of capital in the economy.

Consequently, the main objective of a recent research project of Matthijs Breugem (Collegio Carlo Alberto) and myself, published in The Review of Financial Studies, is to explore how the growth in assets-under-management by benchmarked financial institutions affects informational efficiency and, in turn, asset prices and investors’ portfolio returns. For that purpose, we develop a novel theoretical framework that explicitly accounts for the information choices of institutional investors that are concerned about their performance relative to a benchmark. In the model, investors not only decide on their optimal portfolio but also decide how much capital they want to allocate to the acquisition of private information.

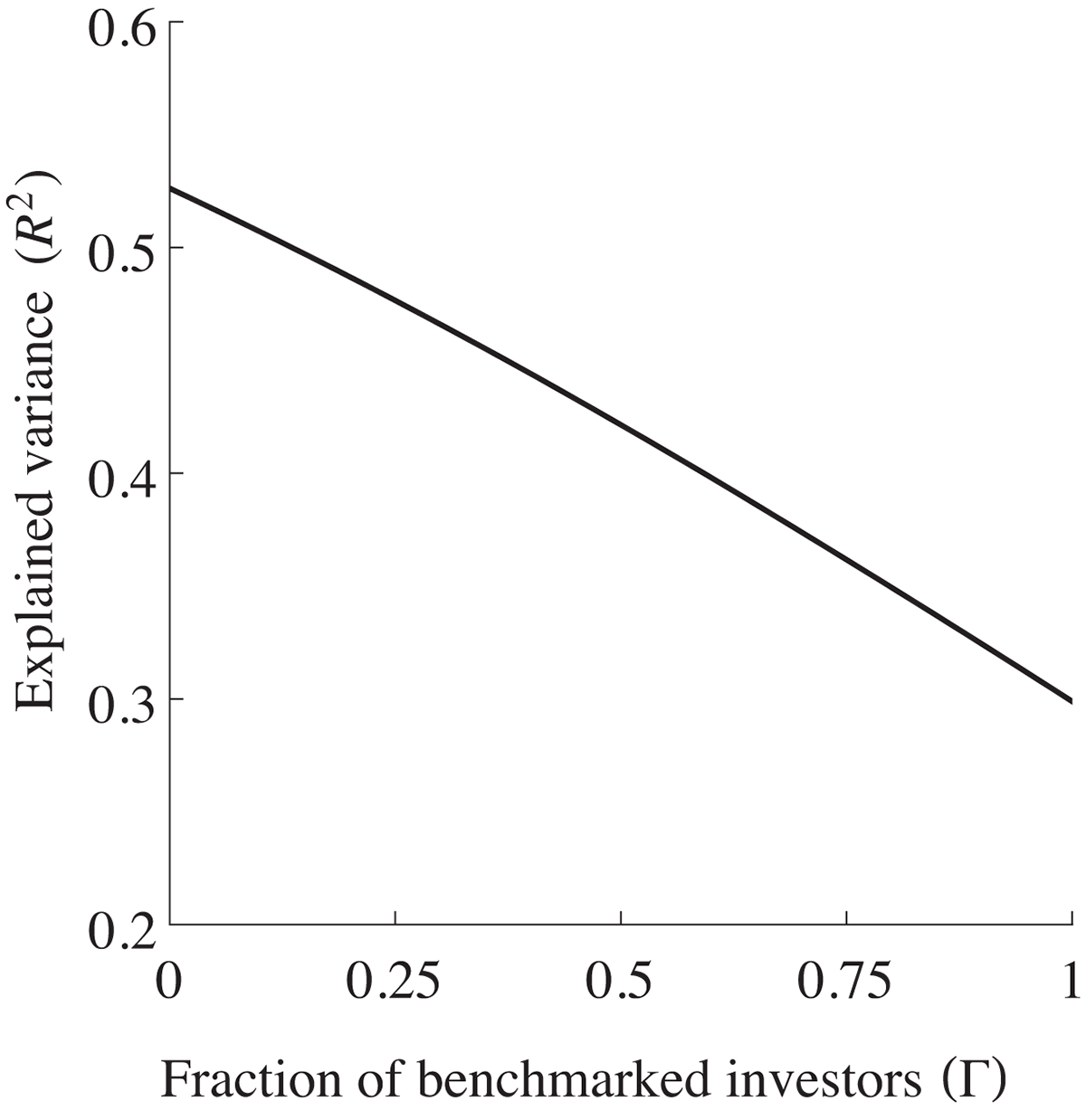

We document two distinct economic mechanisms through which benchmarking affects the information content of financial markets. First, due to benchmarking concerns, institutional investors use a part of their portfolio to replicate the benchmark which, consequently, does not benefit from (more precise) private information.

As a result, private information can only be applied to a smaller fraction of the portfolio which reduces its value. Hence, benchmarked financial institutions invest less in information acquisition. Second, benchmarked institutional investors are less “aggressive” in their use of private information. That is, they trade fewer shares for a given piece of information so that – with each trade – less of the available private information gets incorporated into prices.

Both effects imply a reduction in informational efficiency as the assets-under-management of benchmarked institutional investors increase, as illustrated in the Figure. In particular, while the first effect implies that less private information is available in the economy, the second effect implies that less of the available information gets incorporated into stock prices. Ultimately, all investors can infer less about fundamentals from stock prices; a prediction that is consistent with empirical evidence on the impact of Exchange Traded Funds (ETFs) on stock-price informativeness (Israeli, Lee, and Sridharan, 2017).

This reduction in informational efficiency has important implications for asset prices and the performance of fund managers. For example, because stock prices track fundamentals less closely, stock-price fluctuations are more pronounced, that is, stock-return volatility goes up. Moreover, because institutional investors that are more concerned about their benchmark acquire less information, they earn lower average portfolio returns than their less-benchmarked (i.e., more active) peers.

In summary, our work demonstrates that the growth in assets-under-management by benchmarked financial institutions reduces informational efficiency. As such, it highlights a novel tension between benchmarking as a tool to align the incentives between fund managers and their clients and its adverse effects on individual managers’ portfolio returns and informational efficiency.

This work has received financial support from the Europlace Institute of Finance, the Labex Louis Bachelier and the ‘Asset Management Academy – An initiative by Paris Dauphine House of Finance, EIF and Lyxor International Asset Management’.

References

Basak, S., and A. Pavlova (2013) “Asset Prices and Institutional Investors”, American Economic Review, vol. 103, pp. 1728-1758.

Breugem, M. and A. Buss (2019) “Institutional Investors and Information Acquisition: Implications for Asset Prices and Informational Efficiency”, Review of Financial Studies, vol. 32, pp. 2260–2301.

Cuoco, D., and R. Kaniel (2011) “Equilibrium Prices in the Presence of Delegated Portfolio Management”, Journal of Financial Economics, vol. 101, pp. 264-296.

Israeli, D., C. M. Lee, and S. A. Sridharan (2017) “Is There a Dark Side to Exchange Traded Funds (ETFs)? An Information Perspective”, Review of Accounting Studies, vol. 22, pp. 1048-1083.

*Please note: This is a commercial profile