Kent Matthews, Cardiff University and Zhiguo Xiao, Fudan University, discusses whether new Chinese shadow banks are a threat or an opportunity

Chinese shadow banking has come in for a lot of bad press in recent years. The threat of being the cause of financial instability has resulted in the regulatory authorities clamping down on its activities. Our research suggests that this type of regulation can do more harm than good and does little to reduce the potential of financial instability. We argue that a credible Friedman-type monetary rule, price-level targeting, or nominal income targeting policy is more effective in reducing the likelihood of financial instability than heavy-handed regulation.

Shadow banking (SB) relates to all financial services provided by uninsured and unregulated financial institutions. While registered commercial banks and financial institutions must abide by certain rules to protect investors, depositors and borrowers, the shadow banking sector flies under the regulatory radar. Shadow banking in China is distinguished from its Western counterpart in two ways. First, it is much less complex.

Basically, shadow banks are engaged in providing credit that otherwise would have been provided by the regulated commercial banks. Second, it is much more integrated into the regular banking system than in the West. In China, shadow banking has grown enormously over recent years as a result of regulatory and political factors that stem from the reluctance of state-owned banks (SOBs) to provide loans to small to medium-sized enterprises (SMEs), and an ongoing need by provincial government to access funds for infrastructure projects.

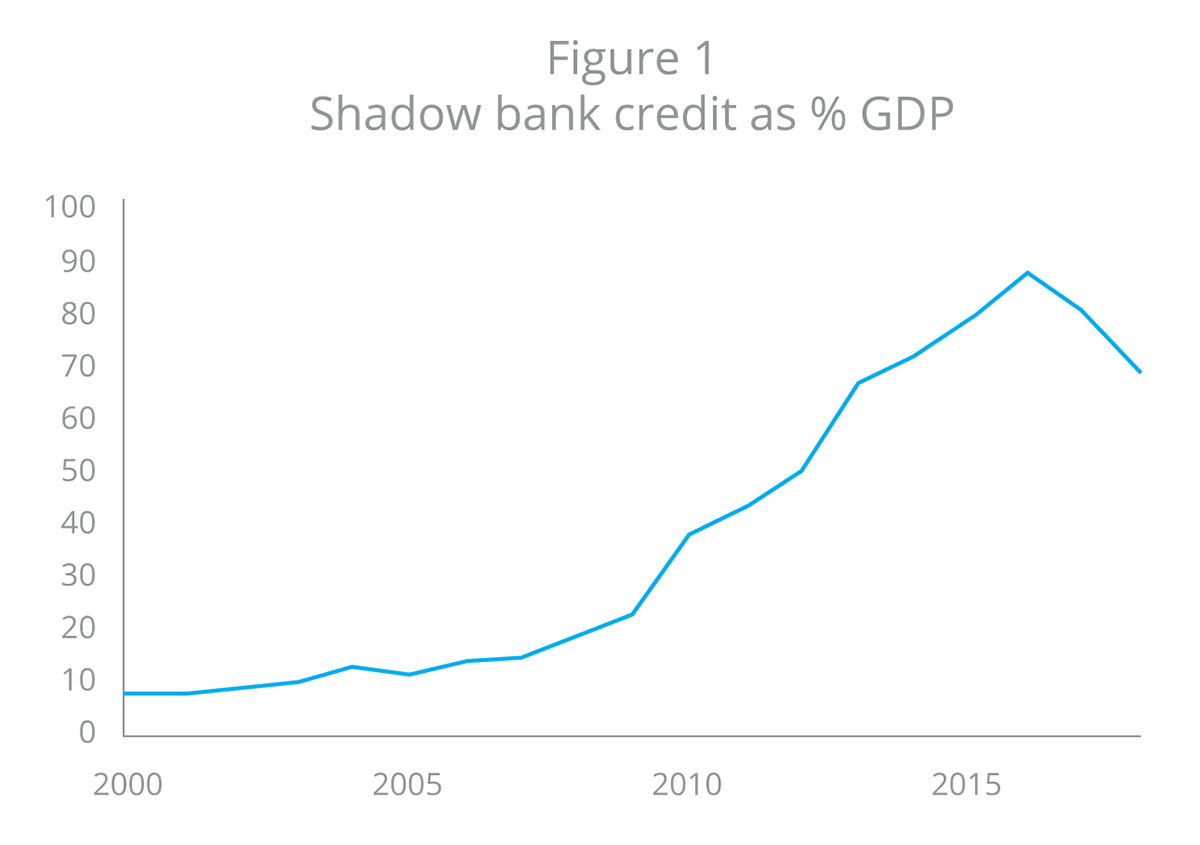

In 2000, SB accounted for less than 10% of China’s economy. It grew rapidly following the Global Financial Crisis (GFC) in 2008/9 and reached a peak in 2016 at over 80% of gross domestic product (GDP). In recent years it has fallen due to increased regulatory pressure (Figure 1).

At first, the growth in SB was tolerated by the authorities as a way of meeting the funding needs of private enterprises and SMEs. However, because of its rapid growth and increase in debt, the SBs have come under stricter regulatory pressure from the authorities, resulting in the closure of thousands of P2P platforms and unprecedented defaults of corporate bonds. The policy of deleveraging the Chinese economy along with a few high-profile fraud activities in the SB sector has prompted the Chinese regulatory authorities to raise the regulatory burden on shadow banks and to squeeze them out of the non-bank financial intermediation business.

Shadow banking has always existed in China in the form of pawn shop lending and rural credit cooperatives, but these entities were too small to pose any threat to the formal financial sector. As Figure 1 shows, the explosion in growth came after the Chinese government stimulus package of RMB four trillion following the onset of the GFC. The fiscal component of the stimulus package was relatively small, and the bulk of the stimulus came in the form of bank loans. Bank credit exploded and in 2009 was growing at the annual rate of 35%.

Much of this credit explosion was directed towards property development and infrastructure spending by local governments. To meet the credit growth ordained by state policy the commercial banks increased their use of off-balance sheet methods such as wealth management products. This is a type of liability management that enabled the increase in funding by avoiding the normal deposit route because of government controls on deposit rates and also for avoiding costly capital charges.

Much of shadow bank lending is also done through state-run organisations. SOBs have been the main supplier of wealth management products and State-owned enterprises (SOEs) have on-lent excess liquidity available to them at preferential rates to SMEs and other private enterprises. This highlights the inter-connectedness of shadow banking in China with the formal commercial banking system.

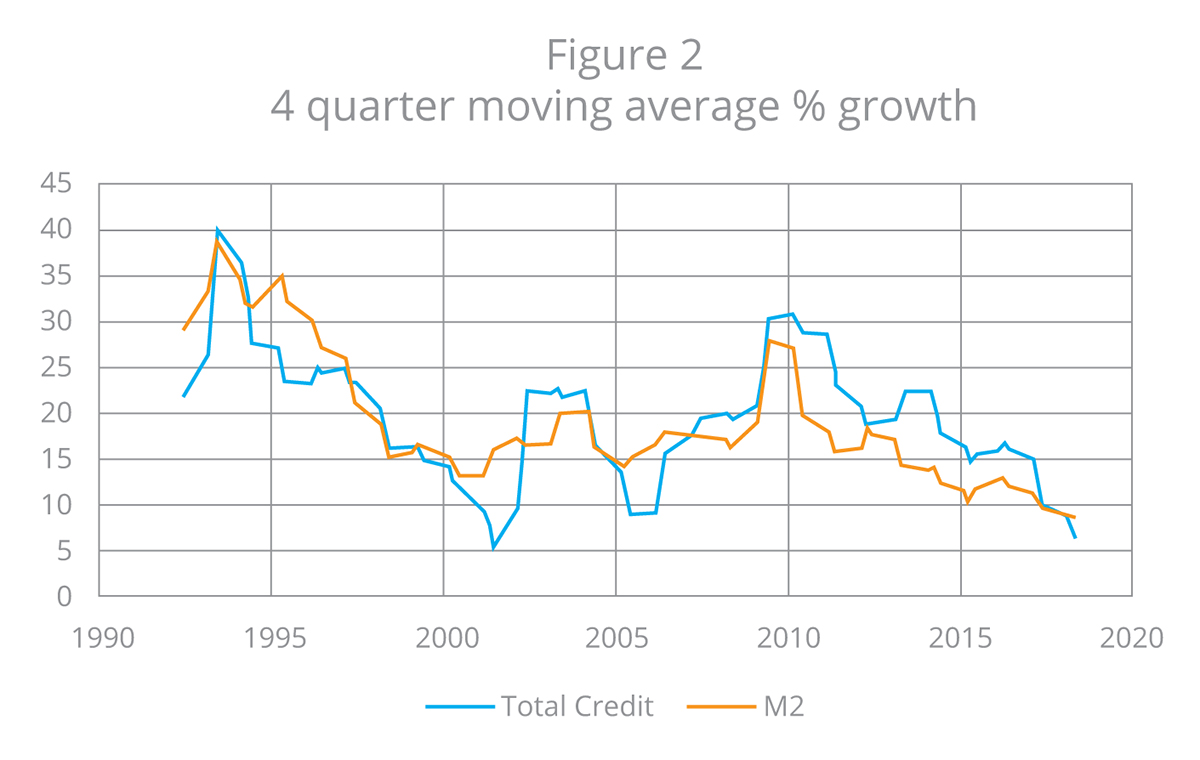

Furthermore, since these SB entities are not deposit taking institutions, they hold their funds in licensed banks as commercial deposits. Hence SBs are not liquidity creators – they do not increase liquidity, but they are liquidity distributors. The difference between the lending by the regular banks and the SBs is that the latter are lending to more risky ventures. Figure 2 shows the rate of growth of total credit, which is the sum of bank credit and SB credit. The differences in growth rates are due to double counting as not all SB funding is from off-balance sheet vehicles as some direct lending by the banks to SOEs are on-lent to SMEs.

The rapid growth of credit alarmed the authorities who saw this as uncontrolled leveraging that will create greater fragility in the economy. Their reaction has been to introduce extra controls on the growth of shadow banking which has slowed its continued growth. But the danger of excessive regulation is that it could do more damage than intended and end up harming the positive outcomes that follow the development of shadow banking.

Our research is distinguished by its methodology which employs the method of indirect inference to estimate and test a macroeconomic model as opposed to the popular Bayesian method. It shows that increased controls cause distortions to the economy that inhibit the growth of the productive SME sector, and doesn’t necessarily reduce the potential of financial instability. We find that credible and well-designed monetary policy reduces the likelihood of financial instability without the need for heavy-handed regulation that distorts the efficiency of the banking system.

This research is supported by ESRC Newton and NSFC (grant # 71661137005).

Please note: This is a commercial profile

Kent Matthews

Professor of Banking and Finance

Cardiff Business School

Tel: +44 (0)292 087 5855