Professor Yumiko Miwa, Meiji University in Japan, discusses the role of the Institutional Investor in ESG investment chain in Japan

In Japan, the Corporate Governance Code was revised for the second time in 2021. A review of the Tokyo Stock Exchange’s market classifications is also underway at the same time and is attracting a great deal of attention from inside and outside Japan.

The main points of the revision are exercising the functions of the board of directors, ensuring the diversity of core personnel, and addressing sustainability. Following TSE’s market reorganisation, the prime market, which has the strictest listing standards, requires at least one-third of the board of directors to be independent directors.

Revised guidelines

In conjunction with the revision of the Corporate Governance Code, the Guidelines for Dialogue between Investors and Companies were also revised. The revised guidelines include the following items for management judgment: (1) Whether the company’s management strategies and plans appropriately reflect its response to changes in the environment, such as the growing social demand for and interest in environmental, social and corporate governance (ESG) and the Sustainable Development Goals (SDGs); and (2) Whether the company has established a framework for examining and promoting sustainability-related initiatives on a company-wide basis. (2) Does the company have a framework for examining and promoting sustainability initiatives on a company- wide basis?

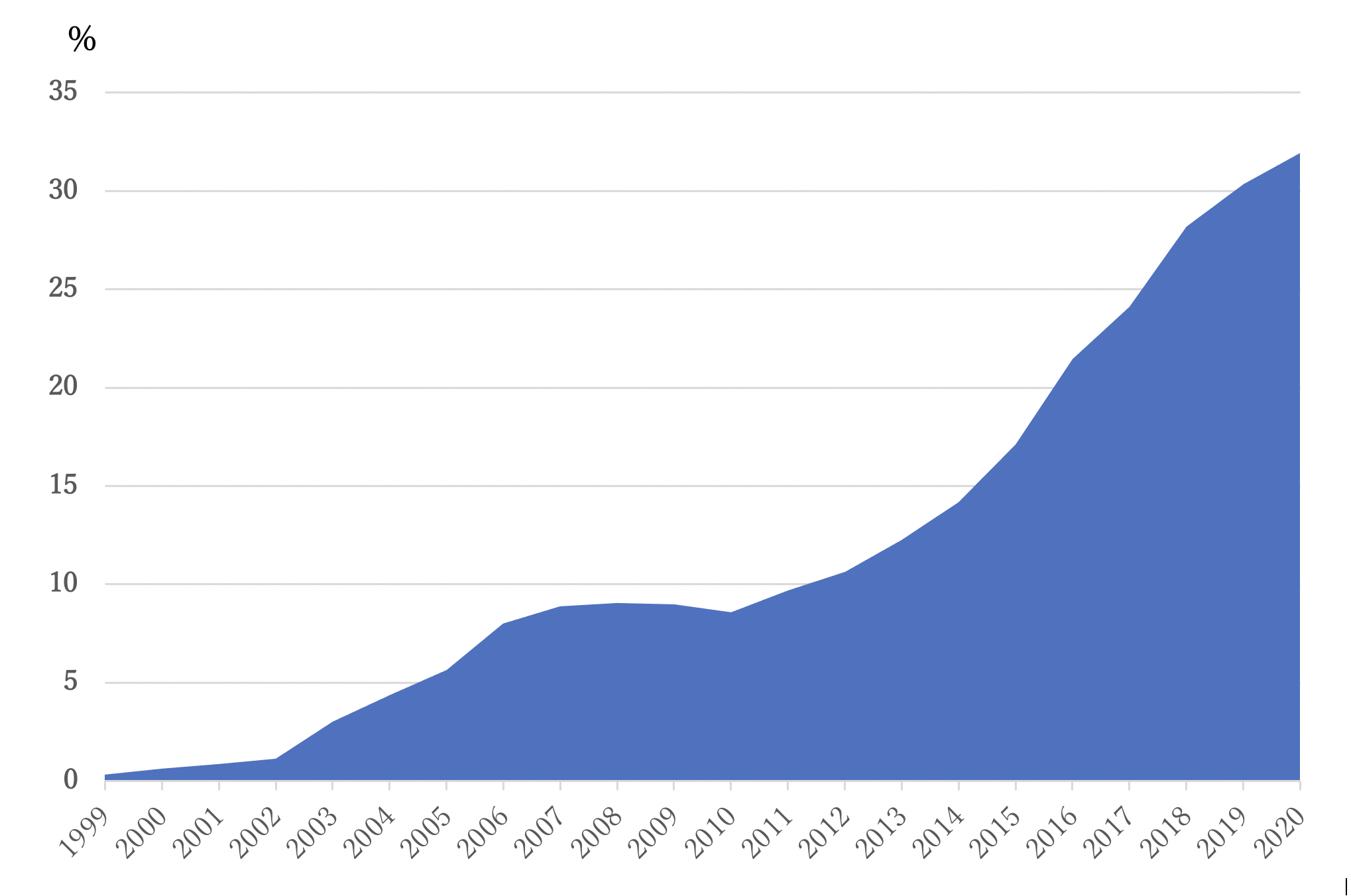

The share of foreign ownership in Japanese companies has been rising and has exceeded 30% in recent years. A more important change has been the rise in the shareholdings of asset management companies. The shareholding ratio of domestic and foreign top 50 asset management companies in the Nikkei 225 stocks in 2021 was less than 1% in 1999 but it will exceed 30% by 2020 (See Figure 1). Some of the companies in the Nikkei 225 Index have a shareholding of more than 50%. These asset management companies are taking steps such as tightening their criteria for exercising voting rights and have strengthened their engagement (constructive dialogue) since the introduction of the Corporate Governance Code and the Stewardship Code.

In the annual reports of companies, trust banks and master trusts are listed in the major shareholder column and according to data from QUICK FactSet (19 August 2021), 1170 institutional investors, including asset managers, are listed as major shareholders, led by BlackRock and Fidelity and Nomura Asset Management and Nikko Asset Management. The total market value of Japanese shares held by these companies is estimated to be around US$1.6 trillion. The breakdown is almost entirely made up of asset management companies from Japan, the US and the UK and their assets account for nearly a quarter of the capitalisation of the Tokyo Stock Exchange.

A major change over the past 20 years has been the emergence of non-controlling asset management companies as institutional investors. These institutional investors have a fiduciary duty, and they must be aware of the cost of capital in the face of competition. As the assets of institutional investors increase, the demand for returns more than the cost of capital is expected to intensify.

In addition, the growing concern for the environment and society is reflected in Codes and regulations, and both institutional investors and companies are under pressure to address sustainability. It can be said that shareholder primary management is to be aware of the voices of these institutional investors.

Following the revision of the Corporate Governance Code and the Guidelines for Dialogue between investors and companies, some institutional investors tightened their criteria for exercising voting rights. BlackRock Japan has indicated that it will oppose proposals to appoint directors in charge, for example if there is insufficient disclosure of information on climate change risks. In addition, AllianceBernstein and State Street have announced their intention to oppose the appointment of top management, such as when there are no female directors.

SDGs and ESGs

An increasing number of Japanese institutional investors are participating in climate change-related initiatives such as the Net-Zero Asset Owner Alliance and the Net-Zero Asset Manager Initiative, and they are using corporate disclosure information to exercise their voting rights and Engagement pushing for carbon neutral in their portfolio companies.

Sumitomo Mitsui Trust Asset Management has tightened its criteria for exercising ESG (Environmental, Social and Corporate Governance) related issues from 2021. If a company does not change even after requesting disclosure of information related to CO2 emissions through dialogue, it will consider opposing a proposal to elect directors.

The SDGs and ESGs have had a boom aspect, with some pointing out the problem of “greenwashing,” pretending to take measures to combat climate change. However, the triple bottom line of corporate social responsibility (CSR) has been discussed since the early 1960s. Corporate decisions and performance should be evaluated based on three indicators: economic, social, and environmental impact.

The growth of civil society with such diverse values has led to the current SDGs and ESGs. Four environmental groups, including the Kyoto-based Climate Network, submitted a proposal on climate change measures to Mizuho Financial Group in 2020, garnering more than 30 percent support. In 2021, the same group submitted a shareholder proposal to Mitsubishi UFJ FG asking the company to include in its articles of incorporation a management plan in line with the Paris Agreement, an international framework, and garnered 23% support.

It means that issues such as population growth, environmental pollution, and human rights, which have been discussed since the 1970s, are finally being integrated into the investment chain.

Essentially, the growth of civil society and its voice will lead to the revitalization of the investment chain. We believe that the way to realize multi-stakeholder management is for institutional investors to utilize the voices of civil society in their engagement in investment chains that include mature civil society.

References

For more detailed information, please refer to the Nikkei Newspaper “Keizai Kyoushitsu” article September 8, 2021.

Please note: This is a commercial profile